A credit score is more than just a number. It’s the gateway to financial opportunities, determining everything from the interest rate on your mortgage to whether you qualify for a new credit card. Despite its importance, many people find the concept of credit scores confusing. In this guide, we’ll unravel the complexities of credit scores, explore how they are calculated, and offer actionable tips to improve yours.

What Is a Credit Score?

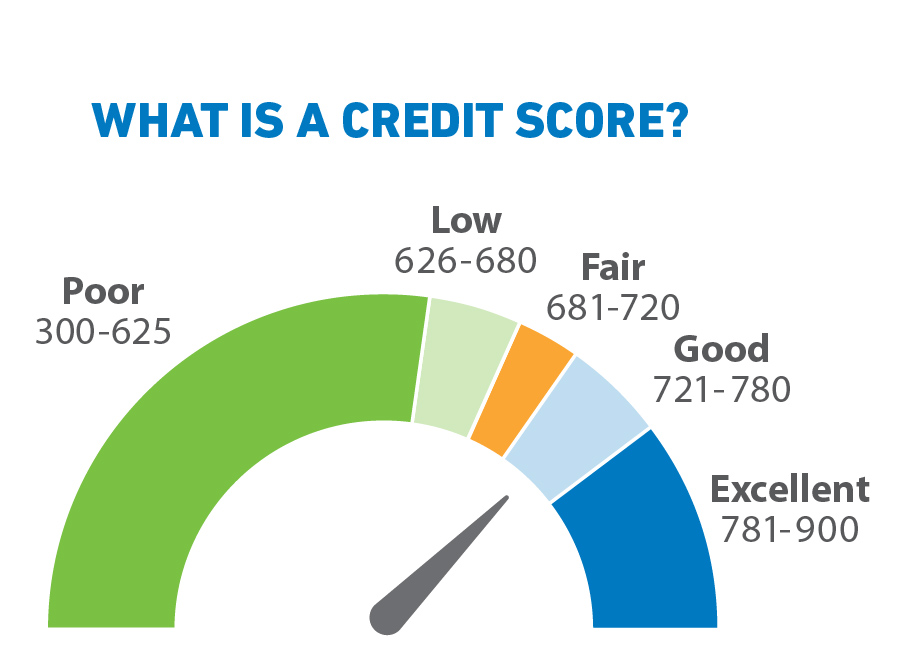

A credit score is a three-digit number that reflects your creditworthiness. Lenders use it to evaluate the risk of lending you money or extending credit. Credit scores typically range from 300 to 850, with higher scores indicating better creditworthiness. The most widely used credit scoring models are FICO and VantageScore.

Your credit score influences your ability to secure loans, credit cards, and even rental agreements. A higher score means lower interest rates and better terms, while a low score can make borrowing more expensive or even impossible.

How Credit Scores Are Calculated

Understanding how credit scores are calculated is crucial for managing your financial health. Both FICO and VantageScore models consider similar factors but weigh them differently. Here’s a breakdown:

1. Payment History (35% of FICO Score)

Your payment history is the most critical factor. Lenders want to know if you’ve paid your bills on time in the past. Late payments, defaults, or bankruptcies can significantly lower your score. To maintain a positive payment history, always pay at least the minimum due on your accounts.

2. Credit Utilization (30% of FICO Score)

This refers to the amount of credit you’re using compared to your total credit limit. A low utilization rate—typically below 30%—is ideal. For example, if you have a credit limit of $10,000 and carry a balance of $2,000, your utilization rate is 20%.

3. Length of Credit History (15% of FICO Score)

The longer your credit history, the better. This factor includes the age of your oldest account, the age of your newest account, and the average age of all your accounts. Keeping older accounts open, even if you don’t use them often, can help.

4. Credit Mix (10% of FICO Score)

A diverse mix of credit accounts—such as credit cards, auto loans, and mortgages—shows lenders that you can handle different types of credit responsibly. However, it’s not necessary to have every type of credit account.

5. New Credit Inquiries (10% of FICO Score)

Applying for new credit results in a hard inquiry, which can temporarily lower your score. Multiple inquiries within a short period can have a more significant impact, so apply for credit sparingly.

Why Credit Scores Matter

Credit scores affect nearly every aspect of your financial life. Here are some areas where your score plays a pivotal role:

- Loan Approvals: Lenders use your credit score to decide whether to approve your loan application. A higher score increases your chances of approval.

- Interest Rates: Borrowers with excellent credit scores are offered lower interest rates, saving thousands of dollars over the life of a loan.

- Credit Card Perks: Premium credit cards with high rewards and benefits often require good to excellent credit scores.

- Renting a Home: Landlords frequently check credit scores to assess potential tenants’ reliability.

- Employment Opportunities: Some employers review credit reports as part of the hiring process, particularly for roles involving financial responsibilities.

Common Credit Score Myths

There’s no shortage of misconceptions about credit scores. Let’s debunk some common myths:

- Checking Your Own Credit Hurts Your Score: Checking your own credit score results in a soft inquiry, which doesn’t affect your score.

- You Need to Carry a Balance to Build Credit: Paying off your credit card balance in full each month is better for your score and helps you avoid interest charges.

- Closing Old Accounts Improves Your Score: Closing old accounts can shorten your credit history and increase your utilization rate, potentially lowering your score.

- You Only Have One Credit Score: You actually have multiple credit scores, as each credit bureau and scoring model may calculate it differently.

How to Check Your Credit Score

Regularly monitoring your credit score is essential for maintaining financial health. You can check your score for free through various methods:

- Credit Card Issuers: Many credit card companies provide free access to your credit score as a perk.

- Credit Bureaus: Experian, Equifax, and TransUnion offer paid credit monitoring services that include score access.

- Financial Apps: Apps like Credit Karma and Mint allow you to check your score for free and provide insights into factors affecting it.

Checking your score regularly helps you spot errors or fraudulent activity on your credit report, which could negatively impact your score.

How to Improve Your Credit Score

If your credit score isn’t where you want it to be, don’t worry. Improving your score is possible with consistent effort and responsible financial habits. Here are some actionable tips:

1. Pay Your Bills on Time

Set up automatic payments or reminders to ensure you never miss a due date. Even one late payment can have a significant impact on your score.

2. Reduce Credit Card Balances

Aim to keep your credit utilization below 30%, and ideally below 10% for the best results. Paying down high balances can quickly boost your score.

3. Avoid Closing Old Accounts

Keeping older accounts open helps maintain a longer credit history. If you don’t use an old credit card, consider using it occasionally for small purchases to keep it active.

4. Limit New Credit Applications

Only apply for credit when necessary. Multiple hard inquiries in a short time frame can lower your score.

5. Dispute Credit Report Errors

Regularly review your credit report for inaccuracies. If you find errors, dispute them with the credit bureau to have them corrected.

How Long Does It Take to Improve a Credit Score?

Improving your credit score isn’t an overnight process, but consistent effort pays off. Here’s a general timeline for improvements:

- Immediate: Correcting errors on your credit report can yield quick results.

- Months: Paying down high credit card balances and consistently paying bills on time can improve your score within a few months.

- Years: Building a strong credit history and recovering from significant negative marks like bankruptcies can take several years.

How Credit Scores Impact Loans and Mortgages

Your credit score plays a crucial role in the terms you receive for loans and mortgages. Here’s how:

1. Interest Rates

A higher credit score qualifies you for lower interest rates, which can save you thousands of dollars over the life of a loan. For example, on a $250,000 mortgage, the difference between a 3% and 4% interest rate could be tens of thousands of dollars.

2. Loan Approval

Lenders have minimum credit score requirements for different types of loans. For example, an FHA loan typically requires a score of at least 580, while conventional loans often require 620 or higher.

3. Loan Limits

With a higher credit score, you’re more likely to qualify for higher loan amounts. Lenders see you as a lower-risk borrower.

Building Credit from Scratch

If you have no credit history, building a credit score might seem daunting. Here’s how to get started:

- Open a Secured Credit Card: Secured credit cards require a deposit, which acts as your credit limit. Use the card responsibly to build credit.

- Become an Authorized User: Ask a family member with good credit to add you as an authorized user on their account. This can help you build credit without the responsibility of managing your own account.

- Take Out a Credit-Builder Loan: These small loans are designed to help you establish credit. Payments are reported to credit bureaus, helping you build a positive history.

- Report Rent and Utility Payments: Some services allow you to report rent and utility payments to credit bureaus, helping you build credit without taking on debt.

Maintaining Good Credit

Once you’ve achieved a good credit score, maintaining it requires ongoing effort. Follow these tips to keep your score high:

- Monitor Your Credit Regularly: Stay vigilant about changes to your credit score and report.

- Keep Balances Low: High credit utilization can quickly lower your score.

- Pay Bills on Time: Timely payments are essential for maintaining good credit.

- Plan for Major Purchases: If you’re planning to take out a loan or mortgage, avoid activities that could lower your score, such as opening new credit accounts.

A credit score is a fundamental aspect of financial health. It opens doors to better financial opportunities, from securing loans to enjoying lower interest rates. By understanding how credit scores work, actively monitoring your credit, and adopting responsible financial habits, you can achieve and maintain a strong credit score. Whether you’re building credit from scratch or looking to improve an existing score,

What do you think about ?